5. The Paymaster and Issuer Revenue Sharing

A blockchain optimised for stablecoin payments must solve two economic problems that general-purpose Layer 1 networks do not. The first is on the user side: consumers and merchants cannot be expected to hold a speculative native token simply to pay transaction fees. The second is on the issuer side: at Japan's current reserve yields, issuing a JPY-pegged stablecoin is not, by itself, an attractively profitable business.

MIZUHIKI's paymaster addresses both problems simultaneously — it is a distinctive architectural feature of MIZUHIKI and a prerequisite to become a key default settlement rail for JPY-denominated stablecoin transactions in Japan.

5.1 The Structural Problem for JPY Stablecoin Issuers

Any JPY stablecoin issuer relying on reserve yields alone will have limited revenues in the modern near-zero interest rate environment in Japan, compared to USD stablecoin issuers. As such, JPY issuers would benefit from a second revenue line that is tied to transaction volume rather than reserve balances.

MIZUHIKI proposes a clean solution: a canonical paymaster that seamlessly enables stablecoins to be used to pay on-chain transaction fees and a built-in mechanism to share a portion of this stablecoin-based fee revenue with the stablecoin issuers.

5.2 Canonical Paymaster Tooling

MIZUHIKI implements a canonical paymaster to be used as a first touch point for retail-facing applications, in particular, for stablecoins. The MIZUHIKI paymaster allows users to seamlessly transact stablecoins and other supported tokens without holding the native MIZU token on MIZUHIKI, which simplifies the onboarding and overall user experience for non-native crypto users.

In practical terms, a user transacting in a compliant stablecoin on MIZUHIKI never needs to hold MIZU. A Paymaster contract sponsors the transaction against the user's stablecoin balance. Gas settlement occurs in MIZU at the validator layer, with the Paymaster handling the conversion via protocol-managed liquidity.

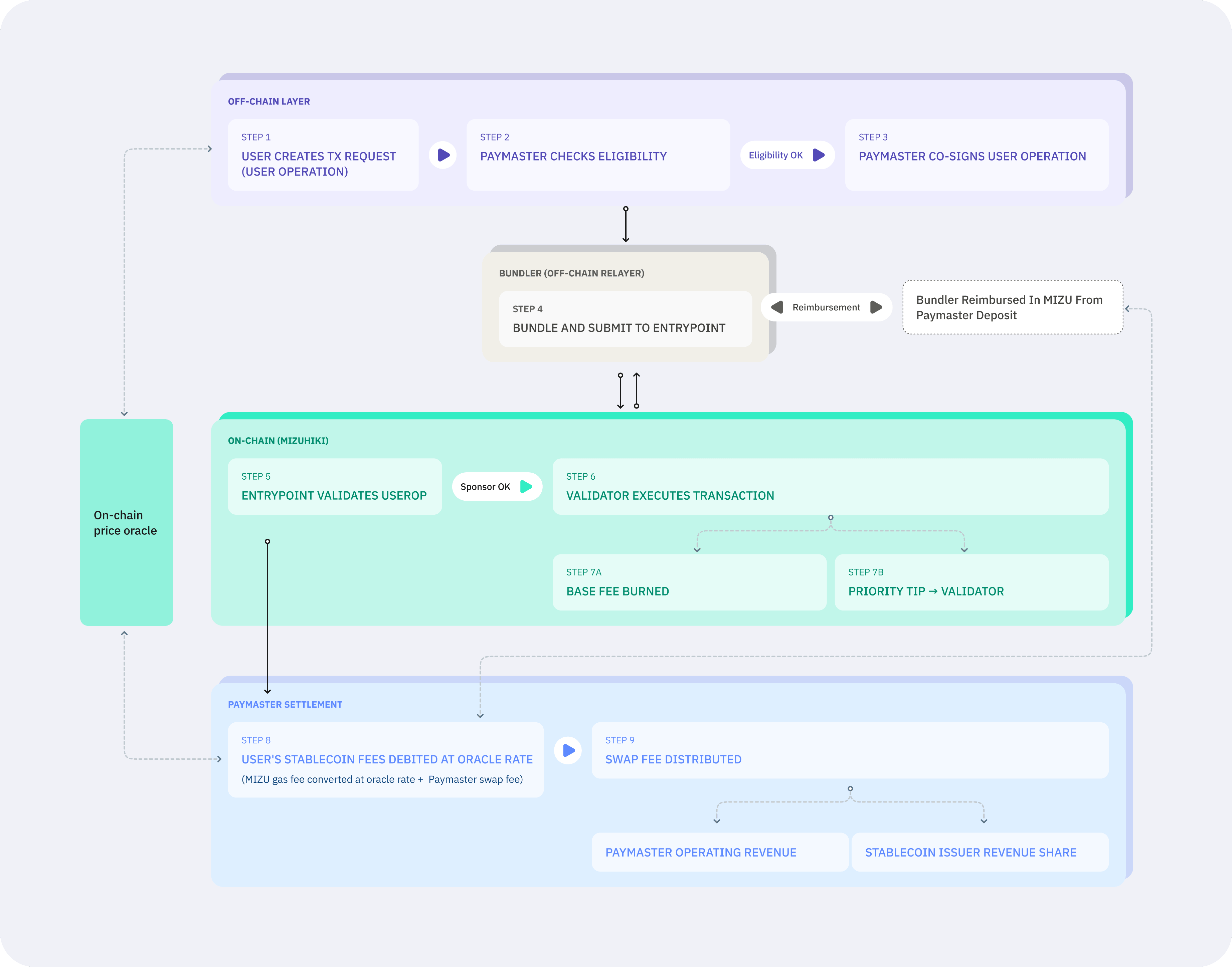

5.3 Gas Payment Flow

A typical transaction on MIZUHIKI proceeds in the following sequence:

- The user signs a UserOperation specifying the transaction to execute and the stablecoin denomination in which fees will be paid. No native MIZU is required of the user.

- The Paymaster checks eligibility against Compliance Suite rules — eligible stablecoin, policy limits, and any issuer- or application-imposed restrictions on the sender.

- With eligibility confirmed, the Paymaster co-signs the UserOperation, committing to settle gas in MIZU on the user's behalf against its on-chain deposit.

- An off-chain bundler aggregates co-signed operations and submits them to the EntryPoint contract on MIZUHIKI. The bundler is reimbursed in MIZU from the Paymaster's deposit, so it never needs to hold the user's stablecoin.

- The EntryPoint validates the UserOp, verifying the user signature, the Paymaster co-signature, and that the Paymaster's deposit covers the maximum gas cost before allowing execution.

- The validator executes the operation. EIP-1559 fee mechanics apply: a base-fee component and an optional priority-fee component, both denominated in MIZU at the protocol layer.

- Protocol fees settle in MIZU: a) The base fee is burned, removing MIZU from circulation and preventing collusion between validators and users, consistent with Ethereum's EIP-1559 design. b) The priority tip flows to the block-producing validator, preserving the staking yield that underwrites validator security.

- The user's stablecoin balance is debited by the Paymaster at the on-chain oracle rate, covering the MIZU-denominated gas fee plus a Paymaster swap fee.

- The swap fee is distributed: a share is routed on-chain to the stablecoin issuer whose token was used to pay for the transaction, with the remainder accruing to the Paymaster as operating revenue.

The user experience is in-line with modern payments: sign once and pay in the currency you hold, without the need for a separate gas token. In general, the user need not even know that a blockchain is involved, that account abstraction exists, or that MIZU is the underlying settlement token. This complete abstraction of the native token from the payments user experience is a prerequisite for mainstream retail payments at scale.

5.4 Stablecoin Issuer Revenue Sharing

MIZUHIKI routes a portion of on-chain transaction fees denominated in a given stablecoin back to that stablecoin's issuer.1

The intended effect is to encourage regulated JPY stablecoin issuance in the persistent low-rate environment. A secondary effect, beneficial to issuers, is that their issuance revenue scales with transaction volume, not solely with yield on the reserve balance.

By consequence, incumbent issuers may be energised by business plans that encourage network effects — such as payments and point incentives — similar to existing card networks today.

5.5 Implications for MIZU Token Economics

The paymaster does not weaken MIZU's role in the network. On the contrary, every stablecoin transaction on MIZUHIKI creates demand for MIZU at the settlement layer through three distinct channels.

Base fees continue to burn. Every transaction, regardless of the stablecoin used at the user interface, results in MIZU being destroyed. This creates deflationary pressure on MIZU supply that is directly proportional to network activity.

Validators continue to earn in MIZU. Priority fees and validator rewards flow to validators denominated in MIZU. This preserves the staking yield that underwrites validator security and maintains the alignment between validator incentives and network activity.

Paymaster liquidity is MIZU-backed. The conversion layer between user-facing stablecoin gas and protocol-level MIZU settlement requires MIZU liquidity, provisioned by the Foundation and MIZUHIKI-approved market makers. MIZU therefore functions as the reserve asset of the network's fee market, even while end users transact exclusively in stablecoins.

The net effect is that MIZU captures value from transaction volume even when end users never hold the token directly. Holders benefit from network activity without the network's growth being gated by end-user willingness to hold a speculative asset — a trade-off that has materially constrained payment adoption on other general-purpose Layer 1 networks.